Rising Rates, Prices Shrink Buyer's' Budgets

Realtors aware of the gap between purchasing power and median sale prices in many Florida markets can better assist buyers by finding alternatives.

ORLANDO, Fla. – Typically, the most important question prospective homebuyers need to answer is how much they can afford each month. This number then translates into their “purchasing power”, or how much house that monthly payment can get them. Then, this gives the buyers their price range or budget when they start working with a Realtor® to find a home that meets their needs in practicality and price.

While income and debt have traditionally been the primary factors influencing a person’s purchasing power, recent years have seen another significant, uncontrollable factor come into play – interest rates. Worse yet, at the same time purchasing power is diminishing, the median sale price for homes has increased, leaving some potential buyers unable to budget for the cost of a home today.

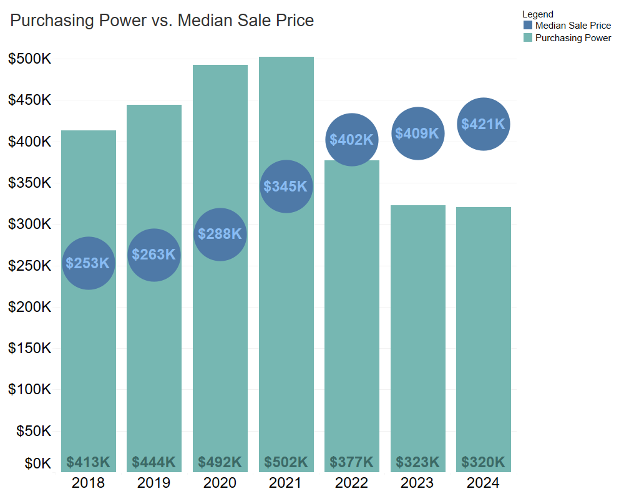

To illustrate this diminished purchasing power, consider this chart showing how much a buyer could afford with a $2,000 monthly budget and 5% down.

A 2018 buyer (with the previous parameters and 2018 interest rates) could afford a single-family home with a max price of $413,000. The average median sale price that year was $253,000, so there was plenty of room for a person to safely afford a median-priced home. As time goes on, the equation still works out, though with a little less buffer in 2021 due to a sharp increase in home prices. Historically low interest rates that year helped keep the equation in check.

Once higher interest rates took hold in mid-2022, the median sale price for the year exceeded what someone would be able to afford on that $2,000 a month budget. Keep in mind, this doesn’t include HOA fees, property taxes and insurance, which also increased significantly. These conditions worsened in 2023 into 2024, as stubbornly high prices met high interest rates, putting what most buyers could afford below the cost of a median-priced home.

Source: Florida Realtors, Freddie Mac 30-Year Fixed Rate Mortgage Average. Estimated purchasing power with a $2,000 monthly budget and 5% down payment. 2024 figure is through June 2024

The impact of the disconnect between what people can afford and what houses cost is twofold:

- The overall number of transactions has declined as fewer buyers can afford today’s prices due to higher monthly costs from current interest rates. The number of closed sales continues to contract, but hasn’t fallen off entirely, which is the second impact.

- Those who can buy in today’s environment are changing, favoring individuals who already own, are moving from other markets and cash buyers. This, of course, leaves first-time buyers, younger local buyers and anyone relying on a mortgage largely out of the buyer pool.

The number of closed sales of single-family homes, condos and townhomes have declined over the past two years due to fewer buyers and higher cost loans on most large consumer purchases. And it appears the current rate environment is here to stay, at least through the end of the year. Some economists believe one and maybe even two interest rate cuts may still be in the cards, but that is not likely to bring much relief to buyers as the market has already baked this into long-term rates.

Knowing the difficulty many face in today’s environment should help you identify alternative options for buyers who still want to get into the market but are up against some significant challenges.

Jennifer Warner is an economist and the Director of Economic Development

© 2024 Florida Realtors®