The 1% Rate Difference on Monthly Mortgage Payments

Florida Realtors economist: Understanding the financial impact of current mortgage rates can help Realtors relate to their clients’ all-important number: their monthly payment.

ORLANDO, Fla. – Interest rate volatility on the 30-year fixed-rate mortgage has dramatically reshaped the housing industry since the onset of the Covid pandemic. Prior to this, interest rates hovered in the 3-5% range in the years coming out of the Great Recession – rates much lower than what was typical in the 1990’s and early 2000’s.

Low, consistent rates helped stabilize an industry that was rocked in 2008-2010 and bring back American confidence in homeownership.

The important part of this long period of stability is that rates were likely in the same range when you went to sell as they were when you bought 5-7 years earlier, the typical tenure for a homeowner in America. This allowed for a nice, fluid market in which the monthly payment amount had more to do with changes in the principal component of the loan than dramatic changes in interest rates.

To prevent another gridlocked economy in the wake of a crisis, though, the Federal Reserve acted aggressively at the onset of the pandemic and reduced interest rates on the 10-year treasury to near zero. Mortgage rates fell quickly too, and the market was thus lit aflame. With everything going sideways, and stimulus money flowing, it was the time to make those moves.

Even people who did not receive a stimulus in the traditional sense via a check from the government were able to receive one by refinancing their mortgage at astronomically lower rates. Prices started to climb, but it didn’t matter on the monthly basis – financing a higher level of debt at a very low rate boosted the purchasing power of consumers across the board – from first-time home to repeat buyers – and everyone was able to gamble with the house’s money.

We’ve discussed the impact of this time extensively in the Florida Realtors News in the past, both as it was happening and a little more recently looking in the rearview as rates started climbing back up with a vengeance in mid-2022. The most significant impact of the rapid change in rates is that the lending environment looks starkly different for those who bought or refinanced in 2020-2022 versus today. The result has been people who are reluctant to relinquish lower rates while concurrently running into a seismic upward shift in prices.

While all these headline numbers matter to real estate professionals and market analysts, what matters to every potential homeowner is the monthly payment. It is often the largest of all the expenses that go on that side of the household ledger and dictates how much is left for the rest of the expenses that make for a life.

It’s easy to forget that a large swing in interest rates on a mortgage can translate into hundreds of dollars more (or less) depending on what they can lock in at the time of the transaction.

It also matters what that monthly payment is in terms of whether a lender will even issue a mortgage, as it may fall outside their stringent debt-to-income ratios. What may have worked when interest rates were around 4% may suddenly not work after rates shot up. Rate hikes rarely could kill a deal before, as they tended to be a few basis points one way or the other from pre-qualification to close. However, over the last 18 months or so, deals died on the vine as the pace of increases was uniquely fast.

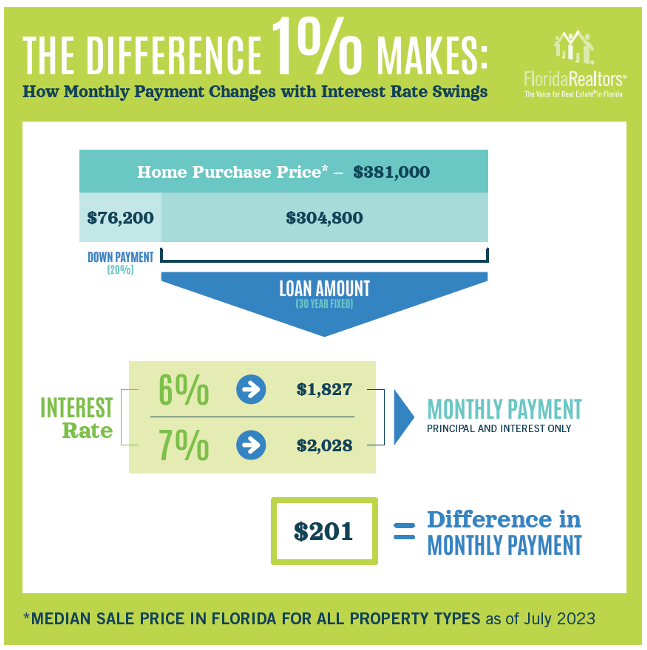

This infographic is a great visual tool to help clients understand the general impact of changes of one percentage point on their monthly payment. Of course, when it comes down to their deal, you will work out the specifics with them based on their circumstances. Still, share this with them to help them understand the general impact of rate fluctuations.

This graphic is designed to communicate shifts in either direction – going from 7% to 6%, (which could happen in the future if rates fall and they qualify to refinance), could result in a reduction in payment by about $200.

Waiting for rates to decrease, however, could backfire if rates continue to climb. What could have been secured at a lower rate could cost $200 more if rates climb.

Test this graphic out on your clients as they come to terms with the environment we’re in today. Help them understand the implications of rate changes and how that could work with their personal finances.

Jennifer Warner is an economist and Director of Economic Development

© 2023 Florida Realtors®