How to Calculate Estimated Mortgage Payments for Buyers

Whether you’re a Realtor or a mortgage lender, clients and customers expect you to be intelligent. They want you to give them quick, accurate projections of what they can expect to pay for mortgage, taxes and homeowners’ insurance.

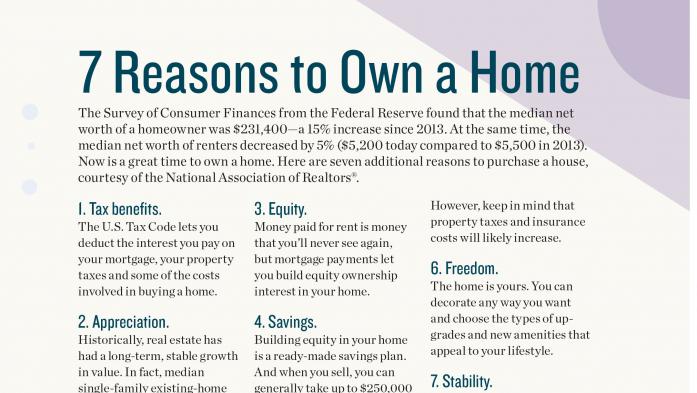

7 Reasons to Own a Home

Cash to close and monthly payments are critical to the consumer purchasing a home. They also want to know you won’t mislead them with ballpark numbers that later prove to be substantially different and even unfavorable. In fact, with all the licensees to choose from, they want your service and your numbers to exceed their expectations if you’re to win their business. If you can do this, you can distinguish yourself. Here’s how:

1. Clearly communicate payments

Don’t disappoint the consumer by saying, “This is your payment, but I forgot to tell you about the other costs associated with the payment.” Quote a payment that includes principal and interest, taxes, insurance, mortgage insurance and homeowners’ association dues.

How do you do that? Here’s my formula: Take 1 percent of the mortgage amount and then subtract $100 or $200 for every $100,000 borrowed. So, if someone is borrowing $100,000, 1 percent of the loan amount is $1,000, less $100 or $200, results in a monthly payment of $800 to $900. You’re also quoting a little high and delivering a little low. If buyers think their payment will be $900 a month and it comes out to $840, they’ll feel great. And you’ll be the hero.

What if someone rents for $1,500 a month? What does that equal in a mortgage? Use the formula backward: Multiply $1,500 by 100, which is $150,000. Then gross it up $10,000 to $20,000. This range reflects the same net range we did when we subtracted the $100 to $200 in the monthly payment estimate. So, they end up with a $160,000 to $170,000 mortgage.

2. Know your area’s taxes

As a starting point, you can use anywhere from 1 to 1.5 percent of the sales or list price. High-cost, expensive subdivisions may be closer to 2 percent. Lower-priced homes are closer to 1 percent. Test it on your farm area. Look at your listing inventory and divide the taxes by the list or sales price to get the tax rate per $100. If the average tax rate is 1.5 percent in your town, you can adjust each rate according to each area — maybe one area is 1.25 percent and another is 1.75.

3. Understand insurance costs

Homeowners’ insurance policies in Florida typically cost about one-half of a percent of the sales price annually. For example, the annual policy for a $200,000 home is usually about $1,000. To get the most accurate figure for your market area, find a sample property or HUD 1 settlement statement and divide the annual policy premium by the sales price. If the policy is $1,200 per year and the house is $200,000, your formula is .60 percent

4. Become a rate expert

One of the questions most frequently asked is, “What are interest rates?” A very astute response would be, “I don’t know what rate you will receive. I do know this: in Freddie Mac’s Primary Market Survey, the 30-year fixed-rate mortgage average was [for example] 3.76 percent last week.” How did you know this? You visited www.freddiemac.com every Thursday and read the one-page weekly news.

5. Identify the Top 5 houses

Suppose your buyers want a house in the $200,000 range in southeast Orlando. You should be able to offer them a list of the top five house values in that range based upon your research and opinion.

Divide your city into quadrants. For example, say there were 3,984 listings in your market. Of those, there were 240 houses in the $200,000 price range. In the quadrant of the city where your customers wanted to buy, there might have been only 32. Of those, you would have been able to identify the top five by using one of three methods. 1. Divide the cost per square foot by the list price. This will give you a numerical value by which you can rank the houses. 2. Personally examine the houses and rank them aesthetically. 3. Rank them by calculating which have the largest difference between the tax assessed value and the list price. When you look at the results of your assessment the top five will be clear.

SOURCE: Adapted from a Florida Realtor magazine article, February 2005.

Author: Grant W. Simon is a loan originator with Waterstone Mortgage in Orlando. In addition to his work in the mortgage banking industry, Simon has served as an instructor for Florida Realtors and Orlando Regional Realtor Association (ORRA).